Financial Modeling with CEV Processes

March 22, 2026

This post is a compact English adaptation of two chapters from my bachelor's thesis. The original thesis text was written in German; this article translates and restructures the core ideas for blog format.

In short: Geometric Brownian Motion (GBM) is the baseline, and the Constant Elasticity of Variance (CEV) model is a useful extension when volatility should depend on the current price level.

Geometric Brownian Motion

Start directly from the stochastic differential equation

Here, is drift, is volatility, and is standard Brownian motion. Under this model, prices stay positive and is normally distributed.

In the thesis, GBM was also built from a discrete random-walk limit argument. That construction is still useful conceptually, but for practical calibration and simulation, the SDE form above is the working definition.

For rigorous background on Itô SDEs, existence, and stochastic integration, see 1.

For daily observations with step size , the log-returns

are approximately normal with

A practical estimator in R:

001log_returns <- diff(log(dax$Price))002sigma <- sd(log_returns)003mu <- mean(log_returns) + 0.5 * sigma^2

This gives immediate inputs for simulation, confidence intervals, and backtesting.

Brownian paths are almost surely not differentiable, so equations like

must be read as integral equations,

This is the precise reason numerical schemes like Euler-Maruyama are used in implementations: they approximate these integrals on discrete time grids 1 2.

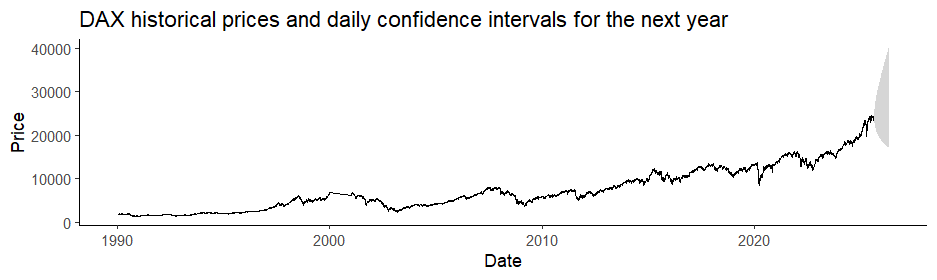

Using the GBM closed form, a two-sided confidence interval for a horizon is

R snippet:

001alpha <- 0.05002T <- 252003z <- qnorm(c(1 - alpha/2, alpha/2))004ci <- S0 * exp((mu - 0.5 * sigma^2) * T + z * sigma * sqrt(T))

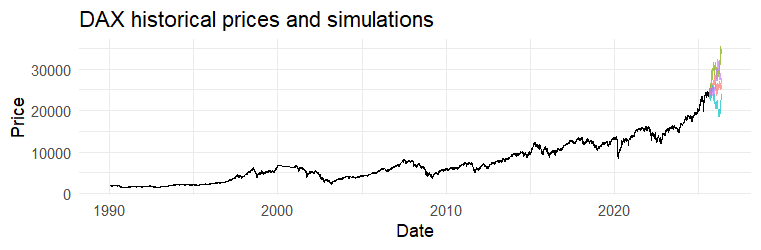

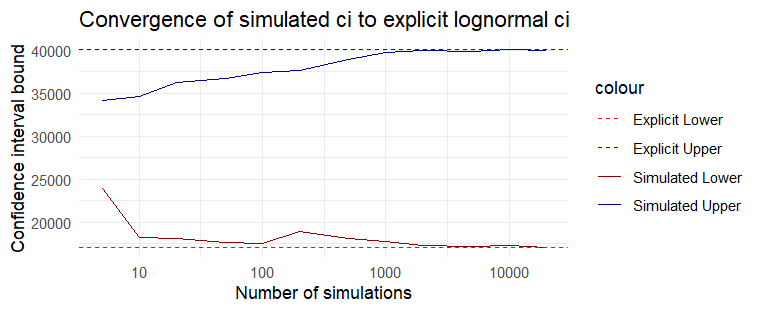

Monte Carlo approximates the same distribution numerically and is the bridge to models without closed forms 3.

001n <- 252002paths <- 1000003S0 <- tail(dax$Price, 1)004005simulations <- replicate(paths, {006 W <- c(0, cumsum(rnorm(n, 0, 1)))007 S0 * exp((mu - 0.5 * sigma^2) * c(0, 1:n) + sigma * W)008})

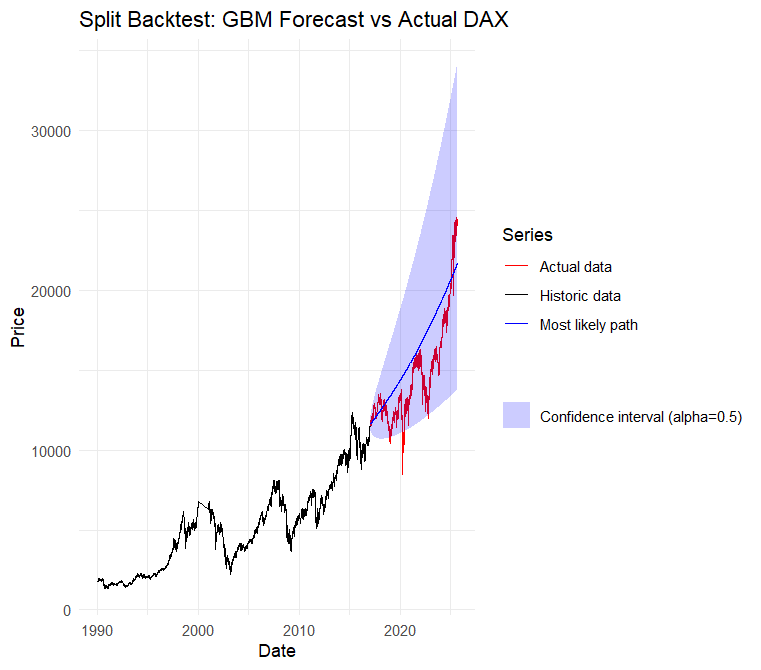

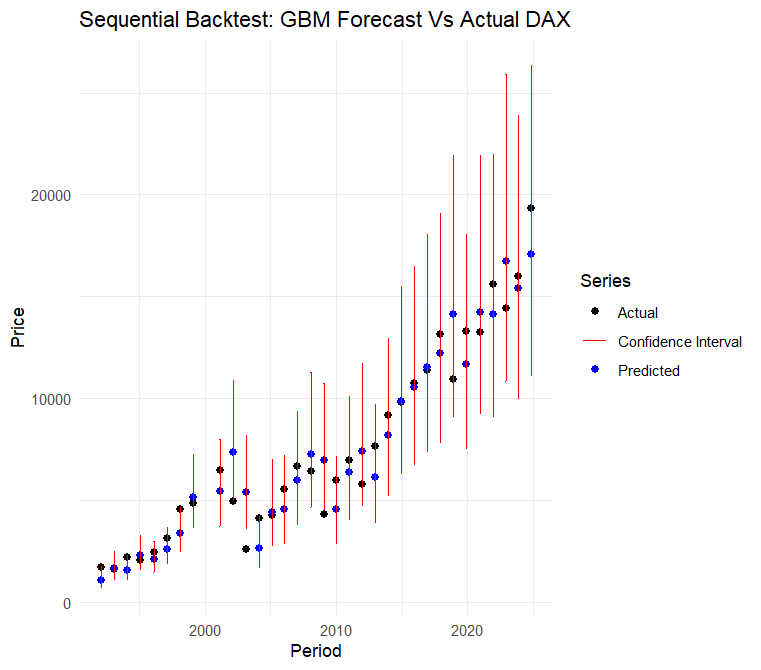

Backtesting answers a practical question: how often do realized values fall into model-based uncertainty bands?

In the thesis setup, calibration on one part of history and testing on a later part produced a coverage measure ("Überdeckungswahrscheinlichkeit" in the German text, translated as coverage probability).

Sequential backtesting repeats this over rolling windows:

The confidence interval formula and Monte Carlo quantiles become closer as the number of simulated paths grows:

The CEV Model

This section corresponds to the second half of Chapter 7 of the thesis (translated from German).

CEV extends GBM by making diffusion state-dependent:

Interpretation:

- : recovers GBM.

- : relatively higher volatility at lower prices.

- : volatility grows faster at higher prices.

So CEV can capture price-volatility coupling that GBM cannot.

For parameter estimation, a common route is Euler pseudo-likelihood (QMLE). With

the Euler step implies

Hence the log-likelihood is approximated by

Then maximize numerically under constraints like and a bounded range.

This is the pseudo-maximum-likelihood route discussed in the thesis and in the SDE inference literature 2.

Simulation (Euler-Maruyama):

001simulate_cev_paths <- function(S0, mu, sigma, beta, dt, nsteps, npaths) {002 S <- matrix(NA, nrow = nsteps + 1, ncol = npaths)003 S[1, ] <- S0004005 for (i in 1:nsteps) {006 Z <- rnorm(npaths)007 S[i + 1, ] <- S[i, ] + mu * S[i, ] * dt + sigma * (S[i, ]^beta) * sqrt(dt) * Z008 S[i + 1, ][S[i + 1, ] <= 0] <- 1e-8009 }010011 S012}

Custom QMLE in R:

001estimate_cev <- function(S, dt = 1/252) {002 S <- as.numeric(S)003 dS <- diff(S)004 S0 <- S[-length(S)]005 eps <- 1e-12006 S0[S0 <= 0] <- eps007008 init <- c(mu = 0.05, sigma = 0.2, beta = 1.0)009010 negloglik <- function(par) {011 mu <- par[1]; sigma <- par[2]; beta <- par[3]012 if (sigma <= 0 || beta <= 0 || beta >= 5) return(1e12)013014 denom <- (sigma^2) * (S0^(2 * beta)) * dt015 denom[denom <= 0] <- eps016017 0.5 * sum(log(2 * pi * denom) + ((dS - mu * S0 * dt)^2) / denom)018 }019020 res <- nloptr::nloptr(021 x0 = init,022 eval_f = negloglik,023 lb = c(-Inf, 1e-8, 1e-6),024 ub = c(Inf, Inf, 4.999),025 opts = list(algorithm = "NLOPT_LN_SBPLX", xtol_rel = 1e-8, maxeval = 3000)026 )027028 setNames(res$solution, c("mu", "sigma", "beta"))029}

The optimizer setup above uses nloptr 4. A package-level alternative is Sim.DiffProc::fitsde 5. The custom estimator is competitive in comparison to the package.

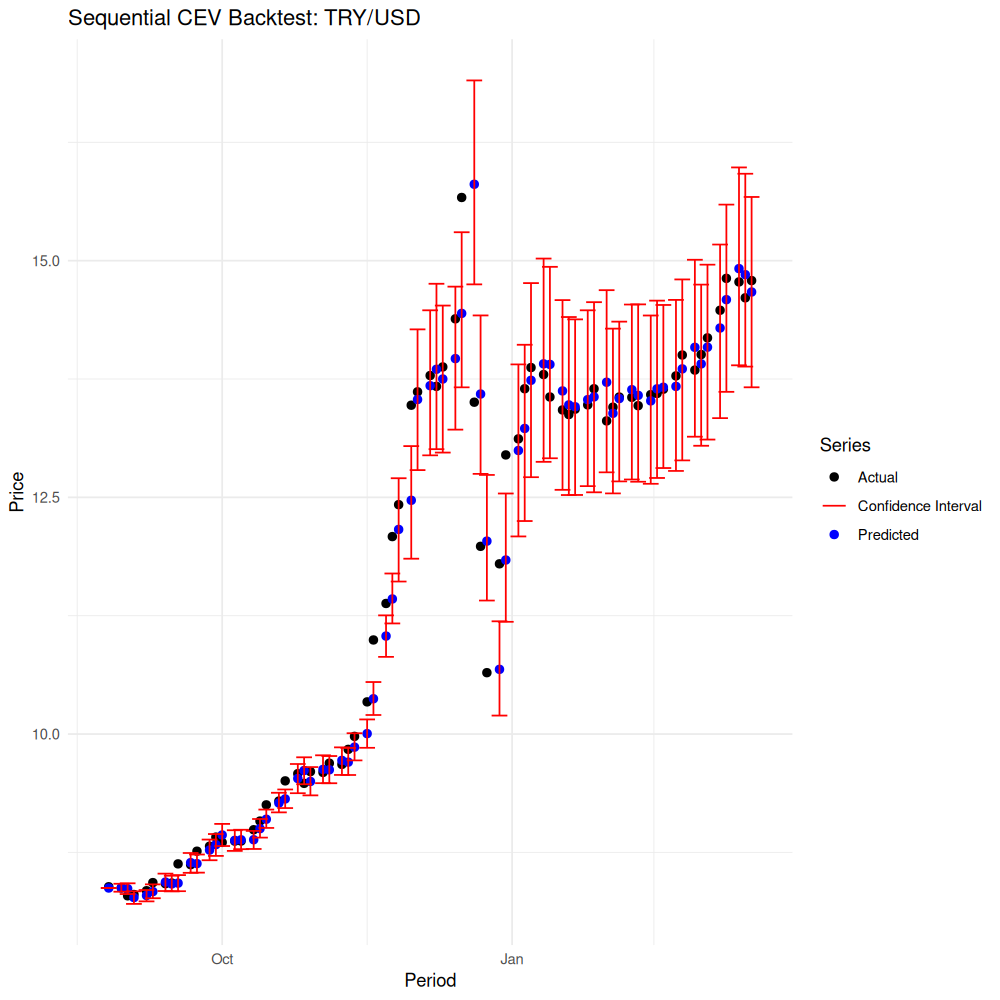

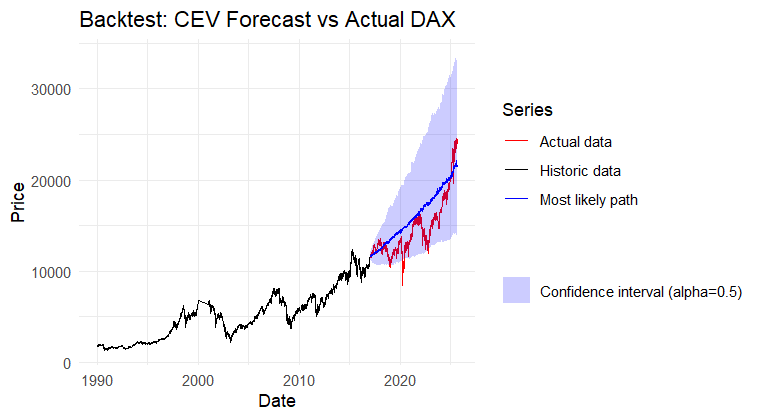

A backtest for the CEV Model:

In this specific dataset, CEV can be close to GBM when is near . In regimes where volatility strongly depends on level, CEV shows clearer gains.

An example from the thesis is a stressed FX period: